'We're being fed this lie': Exposing the myths of Ireland's 'compo culture'

Personal injury awards have been dropping despite suggestions that out-of-control claims are feeding prices.

INSURERS’ SPENDING ON liability and motor claims has barely changed in a decade despite suggestions that Ireland’s rampant ‘compensation culture’ has been behind the country’s recent insurance crisis.

And over the past four years, official awards for personal injuries have fallen significantly – contradicting allegations that growing claim numbers and out-of-kilter payments for minor injuries have fed skyrocketing premiums.

An analysis of insurance and compensation data by Noteworthy, the investigative journalism platform from TheJournal.ie, has found:

- Total awards for personal injury cases fell 28% between 2014 and 2018 in spite of rising premiums;

- The average award dropped 19% during the same period;

- Major insurers’ spending on motor and liability claims barely changed between 2017 and 2013, despite their premium income climbing 57% in the same four years;

- Much higher reinsurance spending – the price of insurers covering risks to their own businesses – rather than higher claim costs has been the largest single factor that has affected firms’ bottom lines in recent years.

Instead of suffering a recent explosion in spending on insurance claims, firms’ costs for motor and liability cases were greater in 2005 than in any year since – although claim costs may take several years to filter through the system.

Stuart Gilhooly, a former president of the Law Society of Ireland, said the narrative that Ireland had a compensation culture rife with high payouts and exaggerated claims was an attempt by insurers to drive down compensation claims to shore up their finances.

“They have very carefully ensured that any claim they see as being fraudulent or where the payout appears too high is emphasised in the media; they have used this as an excuse for why premiums are so high, but that isn’t borne out in reality,” he said.

We’re being fed this lie – and it is a lie – that damages are the main driver of premiums, when quite simply they aren’t.”

Nevertheless, Insurance Ireland CEO Kevin Thompson, whose organisation represents the vast majority of insurers active in the local market, maintained that increased payouts and claims for minor soft-tissue injuries were the main reason for higher costs for customers.

The makings of a crisis

After bottoming out in early 2008, motor insurance prices began their steady climb, almost doubling by mid-2016 before easing around one-third, according to figures from the CSO. Prices are still 48% higher now than at their lowest point just over a decade ago.

While there is no official data on costs for insurance in other areas – such as public or employer’s liability costs for businesses – indigenous firms have for years complained about the rising costs of insurance or, in some cases, difficulty in getting cover altogether.

The crunch in the insurance industry was exemplified recently with the withdrawal of Leisure Insure from the Irish market, leading to concerns that firms in the adventure sector would go to the wall due to higher premiums or their inability to get insurance.

Peter Boland from the Alliance for Insurance Reform, a group made up of various business and voluntary organisations, said it was clear to everyone with an interest in insurance that there was a crisis – but the absence of clear information meant that it was hard to diagnose the cause.

Everything that you’re getting is based on assumptions, and the vast majority of them aren’t backable.”

Compensation culture

With the rapid rise in insurance premiums has come intense pressure on the government from businesses and the public to help put a lid on prices, accompanied by growing anger about spurious claims and seemingly absurd payouts in the courts.

Fine Gael TD Maria Bailey – and her now-infamous fall from a swing at Dublin’s trendy The Dean hotel – became a lightning rod for public angst over high insurance costs and the belief that these were being fed by ridiculous claims.

That, coupled with reports of fraudulent cases being thrown out by judges, led to the common lament that Ireland’s compensation culture had been allowed to run riot.

In May, Minister of State Michael D’Arcy, who has been charged with overseeing insurance reform, complained to the Dáil that “the high level of awards here and the easy money to be made … have given rise to an attitude where people will try to get what they can”.

Business Minister Heather Humphreys was singing from the same hymn sheet a day earlier when she said many firms felt they were “being punished for this compensation culture” of fraudulent or exaggerated claims.

Insurers have put the rate of fraudulent or exaggerated claims in Ireland at around 20% – around half of which they said were caught – a staggeringly large figure which the industry has suggested is responsible for adding €50 to the cost of the average insurance policy.

However Sinn Féin finance spokesman Pearse Doherty punched a sizeable hole in those numbers earlier this year when he highlighted data that showed just 19 cases of suspected insurance fraud had been reported to gardaí in the six months from October.

That would represent a minuscule share of the more than 200,000 motor and liability claims insurers handle every year.

Doherty told Noteworthy that he agreed some insurance cases awards were too high, but the idea that the system was awash with fraudulent claims was a myth that the industry had carefully cultivated.

There is no such thing as an exaggerated claim, it’s industry-speak. An exaggerated claim, as confirmed by the gardaí, is a fraudulent claim … and insurers have a duty to report those fraudulent claims,” he said.

Insurance Ireland’s Thompson said that one-fifth of claims raised some kind of ‘red flag’ as potentially fraudulent or exaggerated.

Of this share, some would be rejected outright, while others would be negotiated based on what insurers thought was a fair offer, he said. Only in “extreme” cases, when insurers could gather enough evidence, was the file typically passed on to An Garda Síochána.

The government-established Personal Injuries Commission, chaired by former High Court president Nicholas Kearns, declared in 2017 that “exaggerated and fraudulent claims contribute significantly to driving up insurance costs”, however its reports did not cite the reason for the conclusion.

A separate 2017 report from the Cost of Insurance Working Group, made up of staff from various State agencies and departments, noted fraud was not one of the main reasons why motor insurance costs had increased so much over the last 12 months.

A follow-up report noted there was no official data to indicate that insurance fraud was widespread.

Minister of State Michael D'Arcy (front) and Finance Minister Paschal Donohoe

Minister of State Michael D'Arcy (front) and Finance Minister Paschal Donohoe

Clusters

Nevertheless, further evidence that some people may be exploiting the insurance system to their benefit has been highlighted in the existence of geographic ‘clusters’ of claims.

Minister of State D’Arcy raised the issue in an interview in December, when he told the Sunday Independent that there were local issues that meant some areas had bigger problems than others with a compensation culture.

According to an analysis of figures from the Personal Injuries Assessment Board (PIAB), the State agency set up to handle personal injury cases, and local authorities, there are significant clusters of claims in parts of the country.

Adjusted for population, Limerick residents were the most likely to receive an award from PIAB over a 10-year period, followed by people based in Longford and Louth.

Limerick residents were more than three times as likely to receive an award than those living in Kilkenny, which had the lowest number of awards per capita.

Similarly, Limerick City and County Council had the highest number of compensation claims by head of population after Dublin City Council over an extended period.

The Dublin figure is likely skewed by the large number of visitors and workers in the capital’s city centre. Longford County Council had the fourth-highest per-person share, behind Waterford City & County Council.

What is not clear, however, is the reason for the disparities – and the extent to which they indicate a compensation culture running rampant in some parts of the country.

Speaking with Noteworthy, D’Arcy said the claim clusters were a cause for concern, although his information had been based on anecdotal feedback from the industry.

If there are clusters, it would suggest that there are people who are gaming the system. And that’s not acceptable, it’s not acceptable because it does damage, it’s closing businesses,” he said.

Whiplash

Since it first met in early 2017, a key focus of the Personal Injuries Commission has been on the incidence and levels of soft-tissue awards – commonly referred to as whiplash claims.

The commission handed down one of its headline findings last year, when a benchmarking exercise revealed that general damages for whiplash injuries were more than four times higher here than in England and Wales.

Average claims involving these injuries were worth €19,862 in Ireland between 2015 and 2017, compared to just €3,798 in the UK for the same period.

The level of these claims in Ireland are ultimately set by the courts, the payouts from which in turn feed into the Book of Quantum, which PIAB refers to when assessing its own awards.

D’Arcy has said the “single most essential challenge” to be overcome in order to bring down insurance costs was to bring down these personal injury awards in line with those in other jurisdictions.

With that in mind, the government is rolling out a range of measures, including a judicial ‘recalibration’ of compensation guidelines, although D’Arcy has sought assurances from the insurance industry that lower payments will also lead to lower premiums.

Claim costs

But there is little evidence that more frequent or higher personal injury payouts are behind the huge increases in insurance costs in recent years – and, in fact, the available evidence points to the fact that overall claim payouts have already been trending down.

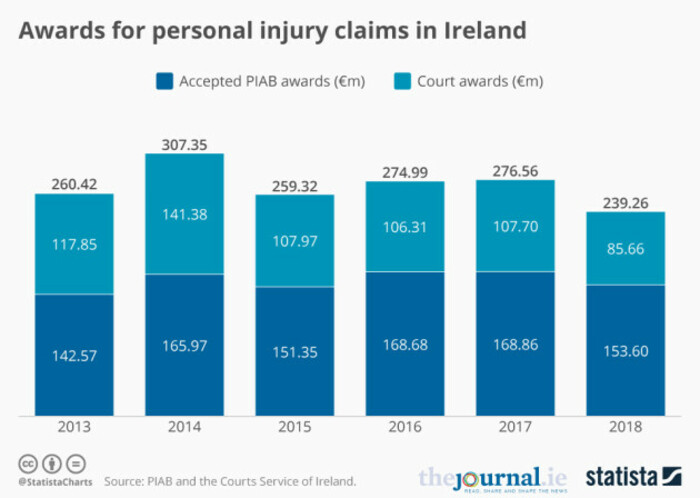

In 2013, some 8,131 personal injury awards were either accepted after a PIAB application or decided by the courts. Last year, this figure was up to 8,351, although both figures are lower than the 8,997 awards decided in 2014.

The total value of all these awards, when medical negligence cases are excluded, was €239 million in 2018, the lowest tally for any of the past six years and 28% below the equivalent figure for 2014.

Claim numbers and payouts for cases in the circuit court – where many soft-tissue claims are heard – have been going up, but these have been counteracted by a reduction in High Court cases and payouts, which account for the biggest share of total awards payable by insurers.

The figures run counter to general trends in the country and economy, in which major gains in employment since the recession have led to more cars on the road, people in workplaces and other factors likely to result in increased insurance claims.

The insurance working group noted in its 2017 report that the available information showed claims had only a “moderate impact” on premiums between 2013 and 2015.

That was despite both the industry and other stakeholders repeatedly pointing to increased claim frequency and costs as the primary reasons for higher premiums, according to the same group.

The black hole in all the publicly accessible data is the large number of insurance claims settled privately between insurance firms and claimants, often through their lawyers. At least 75% of all personal injury claims are thought to be decided in this way.

The majority of these are likely to begin with an application to PIAB, which has seen a steady increase in cases since it was established in 2004. The figures have, however, been largely flat since 2015 despite the pick-up in the economy.

In the absence of more comprehensive information, one of the few clear indicators of how insurance claims have been trending over time comes from insurers’ own finances.

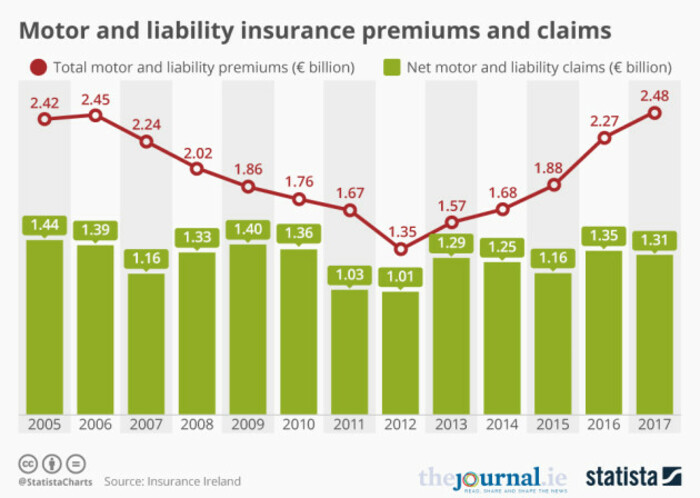

In 2017, the most recent year for which figures are available, motor and liability claims cost insurers a net €1.31 billion, according to Insurance Ireland, whose members represent 95% of the domestic insurance market.

The total includes damage to motor vehicles as the group does not provide standalone figures for personal injury cases. The tally was down on the figure for 2016 but up on the totals for the previous five years.

Nevertheless, it was below the €1.4 billion Insurance Ireland members spent on these claims in 2009, when the firms took in 25% less in motor and liability premiums.

Meanwhile, the share of premiums paid by customers that were flowing out of insurers’ coffers again in claims peaked in 2013. That year, net motor and liability claims were worth about 82% of premiums taken in for the same sectors.

Related Read

By 2017, this ratio had dropped to only 53% – meaning the firms were paying out much less in motor and liability compensation and associated costs relative to their ever-rising premium incomes.

The ratio of net claims to premiums in 2017 was the lowest for any year since 2007.

Back in the black

In recent years, insurers have returned to profit after posting combined losses through the late recession and on into the recovery period.

In 2017, Insurance Ireland members posted an estimated profit of €227 million, up from just €16 million in 2016 and a loss of €216 million a year earlier.

This has led to suggestions from Doherty and others that profit-taking, not claims, was the main reason behind high insurance costs.

However, the recent profits are slender compared to the €1 billion-plus profits the firms recorded in the boom years.

Thompson said firms posting losses was in “nobody’s interest” as ultimately the industry needed to be sustainable to serve its customers, although he disputed claims that excessive profits were being extracted by the industry.

Why then are we seeing insurers particularly international insurers withdraw from the marketplace? Nobody is going to withdraw from a super-profitable market. That, commercially, just does not make sense,” he said.

Nevertheless, with claim payouts little changed over more than a decade, the reason for insurers’ lack of profitability lies elsewhere in their balance sheets – and in the long fallout from the global finance industry’s collective meltdown in the late 2000s.

Throughout the years from 2005 to 2010, insurers paid around 6% of the motor and liability premiums they received from customers back out in reinsurance costs – essentially insurance taken out by the insurer itself to protect against the risks of future claims.

By 2015 that cost had exploded to more than 35% of premiums, leaving insurers with much less money left over from every policy they wrote for the sectors.

Similarly, the collapse in investment returns – particularly for perceived safe investments like bonds – following the global financial meltdown stripped hundreds of millions of euro from insurers’ bottom lines.

Firms are required to hold billions in so-called ‘technical reserves’ for their non-life insurance business to protect them from a raft of future claims. This money also provides an investment return for the business.

In 2017, the investment income on these funds from Insurance Ireland members’ non-life business was just over €100 million – compared to €380 million a decade earlier.

The government’s insurance working group identified this as one of the key reasons for the deterioration in firms’ profitability.

It found the main drivers of increased premiums were underpricing in earlier years, particularly between 2010 and 2014, the costs of keeping large reserves of funds to cover future payouts, and increased claims.

However it added that the available data only suggested claims had a “moderate impact” on prices during the period its figures covered, from 2013 to 2015.

Doherty said the real issue that had led to high insurance premiums was firms with major holes in their finances due to bad investments, and these holes had been filled with “extraordinary” increases in motor and public liability premiums.

Thompson said increased reinsurance costs were an indicator of higher risk in the market.

He added that this risk was being fuelled by insurers anticipating the growing personal injury claims they were likely to receive on current policies in three or more years’ time.

He pointed to industry figures which predicted the average ultimate cost per policy for smaller injury claims had increased 41% between 2011 and 2016.

“The main problem in the marketplace is in soft-tissue claims, and the volume and average payments for those claims have gone up.”

Sinn Fein finance spokesman Pearse Doherty

Sinn Fein finance spokesman Pearse Doherty

The bottom line for customers

Despite the data suggesting reducing whiplash awards and cracking down on fraud will have little overall impact on prices as these make up a relatively small component of total payouts, any cuts in awards should eventually feed into some premium reductions – as long as the savings are passed on to policyholders.

Boland, from the Alliance for Insurance Reform, said businesses believed both insurance awards and claim numbers, particularly for what he referred to as “paracetamol injuries”, were too high.

But he added there was no evidence of increases in these areas that justified the huge premium rises since 2014.

When eventually reform gets over the line, what’s the benefit to the policyholders – what percentage are we going to see premiums reduced? We want to see the numbers,” he said.

For more about how to support Noteworthy’s work, visit our website.